At their core, home mortgages are loans that individuals take out to finance the purchase of a property. These loans are typically large sums of money, and the property being purchased serves as collateral. This means the lender can seize it if the borrower fails to pay.

But, how does a mortgage work? When you take out a mortgage, you agree to certain terms and conditions set by the lender. These terms outline the repayment schedule, including the interest rate, which determines the cost of borrowing the money. Mortgages can have fixed interest rates or adjustable rates.

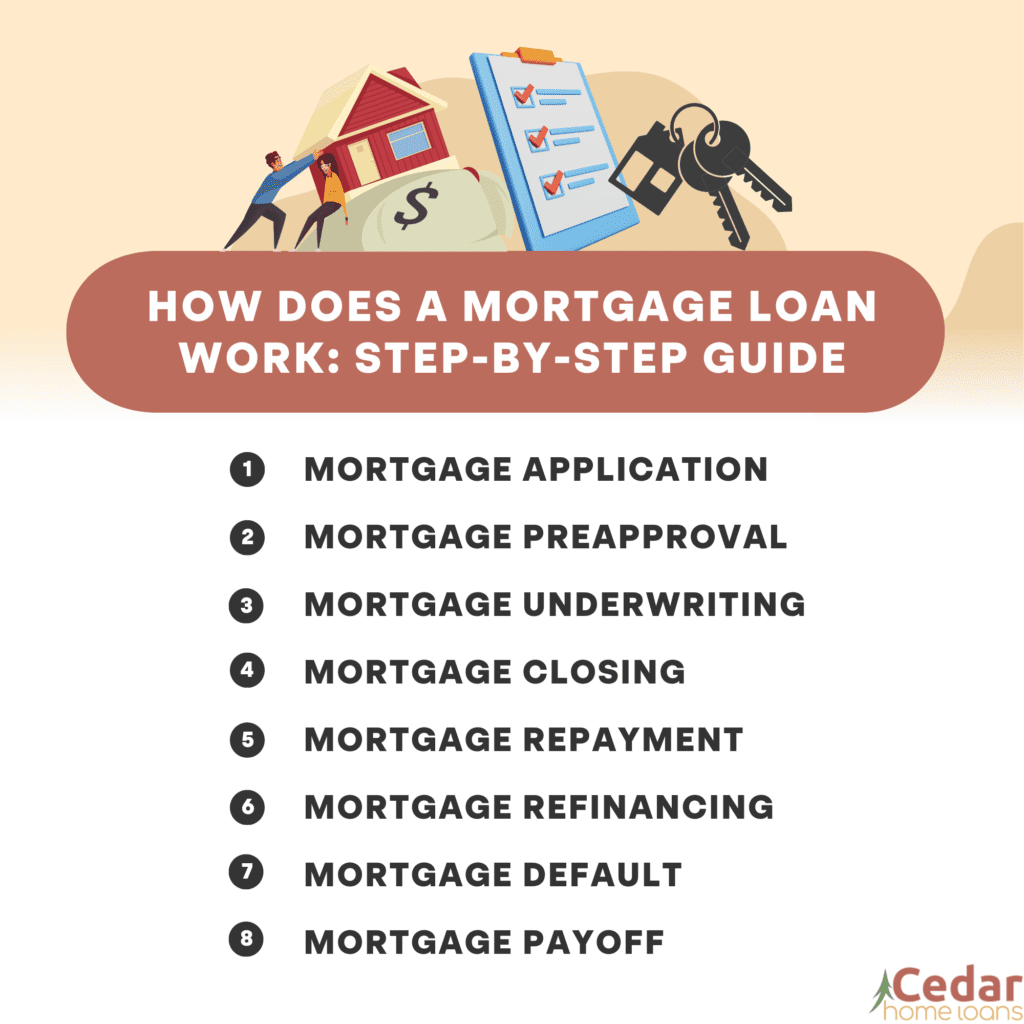

How Does a Mortgage Loan Work: Step-by-Step Guide

Now, let’s dive deeper into the mortgage process. Understanding how mortgages work is crucial to make informed decisions when obtaining a loan for your dream home. Here, we’ll walk you through the essential steps, from application to closing:

1. Mortgage Application

The first step in securing a mortgage is to complete a loan application. During this process, you’ll provide the lender with detailed information about yourself, your financial situation, and the property you wish to purchase. This information may include your income, employment history, credit score, and the amount of money you can put towards a down payment.

The lender will then use this information to assess your creditworthiness and determine the amount of money they are willing to lend you. It’s worth noting that the more favorable your credit score and financial profile are, the more options you will have when it comes to choosing a mortgage.

2. Mortgage Preapproval

Getting a mortgage preapproval can give you an edge when you’re house hunting. It means your financial information has been reviewed and a lender is willing to provide you with a specific loan amount, subject to the property’s appraisal. Preapproval letters from home mortgage lenders are usually valid from 60 to 90 days.

Keep in mind that preapproval is different from prequalification. Prequalification is an estimate of how much you could borrow based on the information you provide to the lender, while preapproval is a more concrete commitment.

3. Mortgage Underwriting

This is when a loan application is evaluated to determine the risk level of lending them money. During this stage, the lender will verify the information provided in the application, such as income, employment, and assets. They may also request additional documentation, such as bank statements and tax returns.

The underwriter will carefully review all the information and assess the borrower’s ability to repay the loan. If the underwriter determines that the borrower meets the lender’s criteria, the loan will move forward in the process. However, if there are any red flags or concerns, the underwriter may request further documentation or deny the loan.

4. Mortgage Closing

This final step of the process is when ownership is transferred to the buyer and all legal documents are signed. During this stage, you’ll be working with a title company or an attorney who will ensure that the property’s ownership is clear and that the lender’s interests are properly protected.

Prior to the closing, you’ll have the opportunity to review the closing disclosure, which outlines the final terms and costs of the loan. It’s important to carefully review this document and double check if this is the same that was offered earlier to ensure that there are no surprises.

5. Mortgage Repayment

Once the loan is closed, you’ll begin making regular mortgage payments. This is usually the principal or the amount borrowed and the interest or the cost of borrowing money. The specific terms of the repayment will depend on the type of mortgage you secured.

Payments for a fixed-rate mortgage are the same all throughout the term. On the other hand, if you have an adjustable-rate mortgage, your payments may change periodically, reflecting any adjustments in the interest rate.

6. Mortgage Refinancing

Mortgage refinancing is an option worth considering when you want to take advantage of lower interest rates, reduce the loan term, or tap into your home’s equity. This means replacing your current loan with a new one either from the same or different lending company.

When you refinance, the new loan pays off the remaining balance on your old mortgage. Then, you make payments on the new loan, just like you did with the original one. However, it’s important to carefully evaluate the costs and potential benefits of refinancing to ensure it aligns with your financial goals.

7. Mortgage Default

A mortgage default occurs when a borrower fails to make the required payments as outlined in the loan agreement. If you find yourself in this situation, it’s important to take action quickly. The exact process and timeline when the lender can foreclose the property depends on the state or terms of the mortgage.

Foreclosure is the legal process through which the lending company can take your property and sell it to recover the unpaid loan and expenses of lending you the funds. To avoid foreclosure, you may have several options, such as negotiating a new payment plan with the lender, applying for a loan modification, or, in some cases, selling the property.

8. Mortgage Payoff

The mortgage payoff is the final chapter in your loan journey. It happens when you’ve made the last payment on your mortgage, and you now own your home free and clear. The lending company can give you a release of lien or satisfaction of mortgage, which is a document that officially acknowledges that the loan has been paid in full.

Congratulations! Achieving a mortgage payoff is a significant financial milestone.

The Bottom Line

A mortgage is a loan that allows you to purchase a home. However, the journey to homeownership involves understanding how home mortgages work and careful consideration of the mortgage process. It includes selecting the right mortgage for your financial situation, completing the necessary steps to secure the loan, and fulfilling your repayment obligations.

Let Cedar Home Loans Help You Navigate the Path to Homeownership!

Remember, every borrower’s situation is unique. So, take the time to explore your options and seek guidance from Dillon mortgage company and other professionals to make the best decision for your needs. Here at Cedar Home Loans, we are committed to helping you understand how a home mortgage works and navigate the mortgage landscape and turn your dream of homeownership into a reality. Contact us today!