Securing a mortgage is one of the most significant financial decisions you’ll make, so finding the right home loan at the best rate is crucial. But with the multitude of options available, comparing rates from different companies can feel overwhelming.

While it may be tempting to jump at the first low rate you see, taking the time to explore and evaluate your options can help you save in the long run. To help you in your quest for the perfect mortgage, we’ve compiled a comprehensive guide on how to compare mortgage rates.

The Different Types of Mortgage Interest Rates

Before we dive into the nitty-gritty of how to compare mortgage rates, let’s first familiarize ourselves with the different types of interest rates you may encounter:

- Fixed-Rate Mortgages: These mortgages provide you with stable and predictable monthly payments through consistent rates all throughout the term of the loan.

- Adjustable-Rate Mortgages (ARMs): Unlike fixed-rate mortgages, after an initial fixed period, the rates can fluctuate. They are typically lower during the fixed period but keep your eyes open on market conditions which can increase or decrease the rates.

- Interest-Only Mortgages: With these mortgages, you have the option to pay only the interest for a specified period. If you plan on selling the property before the principal payment kicks in, this mortgage is ideal for you.

- Government-Backed Mortgages: These are mortgages that the Federal Housing Administration (FHA) and the Veterans Administration (VA) insure and guarantee. They often have competitive interest rates and more flexible qualification requirements.

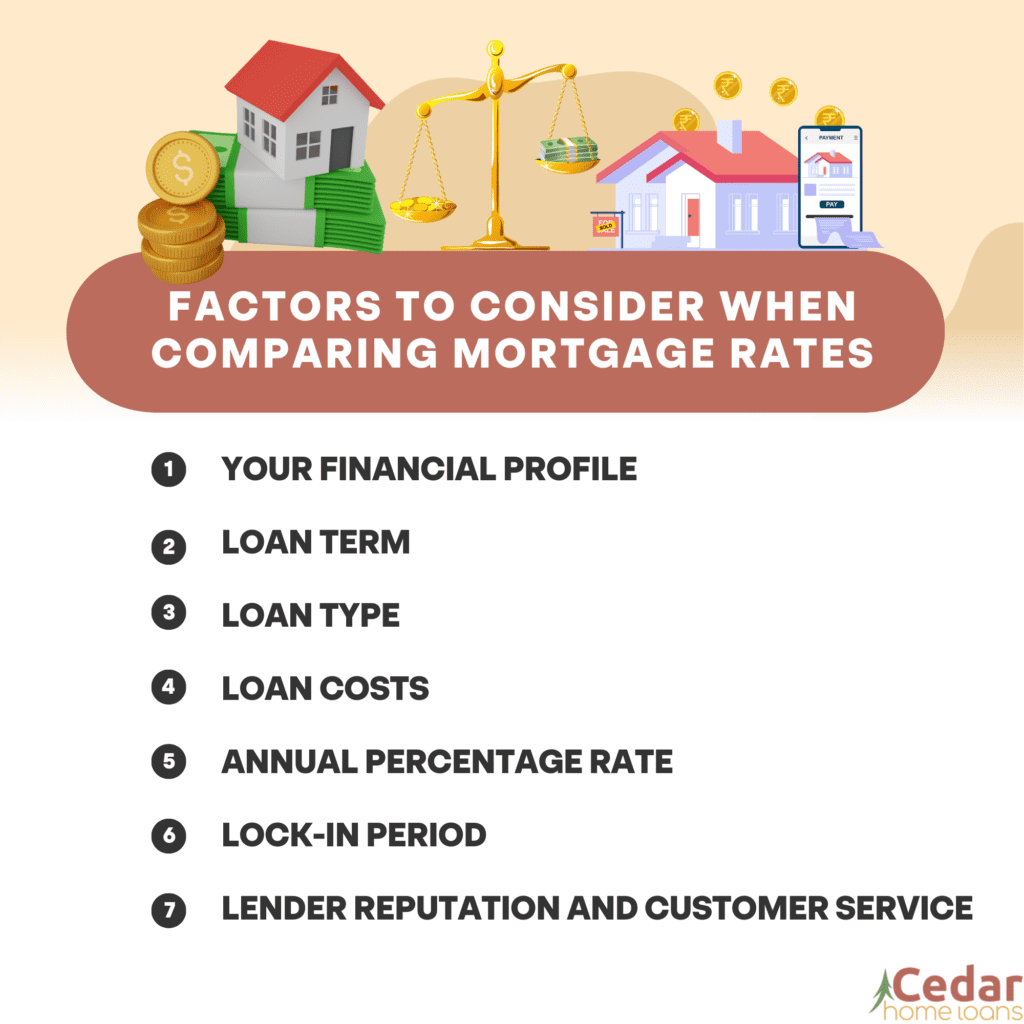

Factors to Consider When Comparing Mortgage Rates

Now that you’re familiar with the different types of interest rates, let’s move on to the essential factors to consider when comparing mortgage interest rates:

1. Your Financial Profile

Your credit score, income, and debt-to-income ratio play a significant role in the interest rate you’ll qualify for. Lower interest rates are available for borrowers with higher credit scores and lower debt-to-income ratios. Before you start shopping for a mortgage, take the time to review your credit report and ensure its accuracy.

2. Loan Term

This is how long you’ll take to repay the mortgage, which can also impact the interest rate. Longer-term mortgages, such as 30-year loans, often have higher interest rates but lower monthly payments.

3. Loan Type

The type of mortgage you choose will also affect the interest rate. Conventional mortgages, which aren’t insured by the government, typically require higher credit scores and offer lower interest rates for borrowers with good credit.

In contrast, government-backed mortgages, like those offered by the FHA and VA, have more flexible credit requirements but may have slightly higher interest rates.

4. Loan Costs

When comparing mortgage rates, it’s important to consider the associated loan costs, including origination fees, discount points, and closing costs. These costs can vary significantly among lenders, so pay close attention to the loan estimates provided and calculate the overall costs for each option.

5. Annual Percentage Rate

The annual percentage rate (APR) takes into account not only the interest rate but also other charges and fees, giving you a more accurate picture of the total cost of the mortgage. When comparing mortgage rates, don’t solely focus on the interest rate; also, consider the APR to determine the best deal.

6. Lock-In Period

If you anticipating the rise of interest rates in the near future protects you from potential increases. However, if rates drop and you have a locked-in rate, you may miss out on potential savings. Carefully evaluate your options and consider current market conditions when deciding on a lock-in period.

7. Lender Reputation and Customer Service

While the interest rate is a critical factor, it’s equally important to consider the reputation and customer service of the lender. A smooth and efficient mortgage process can save you time, stress, and even money. Take the time to read reviews, seek recommendations, and evaluate the responsiveness of potential lenders before making a final decision.

The Bottom Line

Comparing mortgage rates is not just about finding the lowest percentage. It’s a careful evaluation of your financial profile, loan terms, and costs. Remember, what works for one borrower may not work for another, so take the time to assess your needs and financial goals.

Start Your Mortgage Shopping Journey With Cedar Home Loans!

When you’re ready to start your mortgage shopping journey, call the best expert Vail mortgage brokers. We’ll help you navigate the process, compare home mortgage rates, and find the best mortgage rate for your dream home. Contact us today!