What not to say to a mortgage lender can be as crucial as what you say. Here are some things you should avoid when communicating with a lender for a smooth and successful loan application.

Getting a mortgage loan can be a complex and sometimes overwhelming process. It requires careful planning, meticulous documentation, and effective communication with your lender. When it comes to communication, knowing what not to say to a mortgage lender is just as important as knowing what to say.

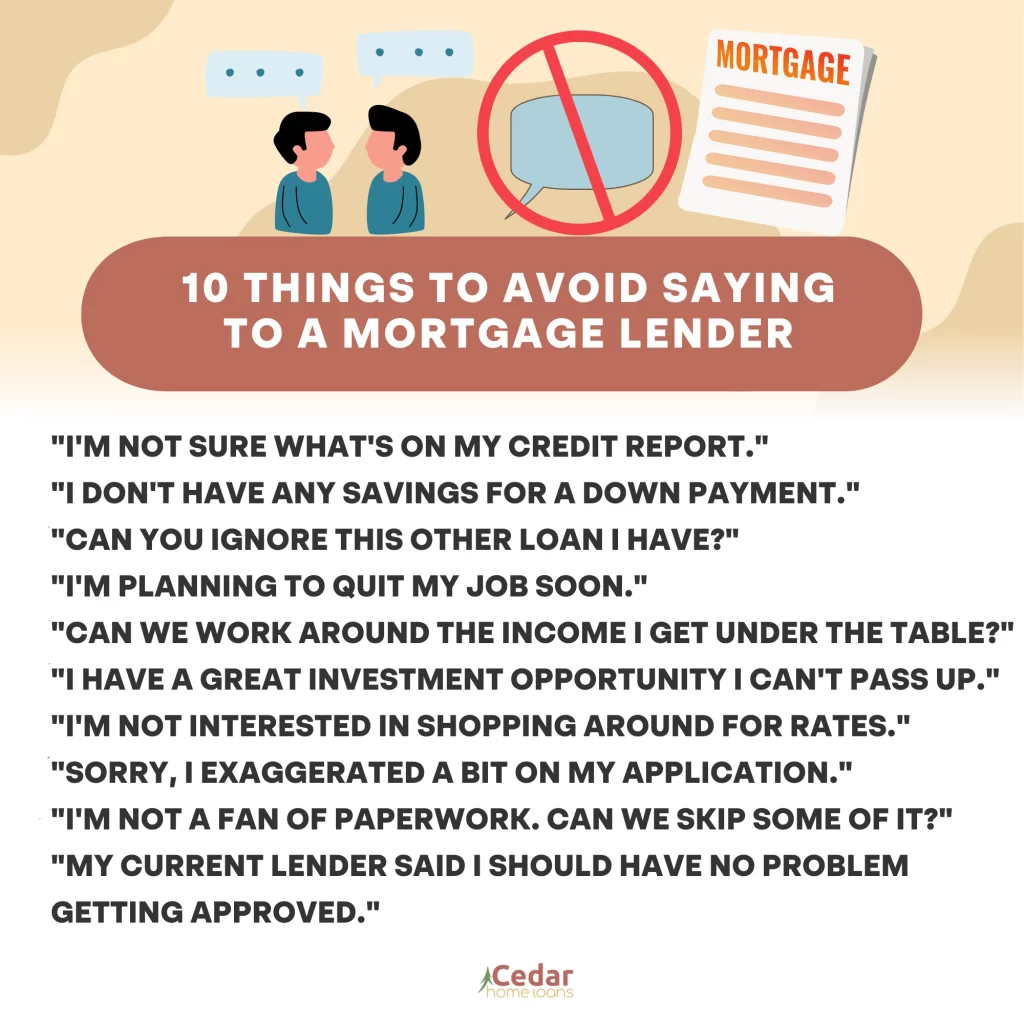

10 Things to Avoid Saying to a Mortgage Lender

Your words can have a significant impact on your loan application, so it’s crucial to choose them wisely. To help you navigate the conversation successfully, we’ve compiled a list of things to avoid saying to your mortgage lender:

1. “I’m not sure what’s on my credit report.”

Having a good credit score is essential for securing a favorable mortgage. When you tell your lender that you’re unsure about the details of your credit report, it raises a red flag. It suggests that you may not be fully aware of your financial situation, which can be a cause for concern.

What to say instead: Take the time to review your credit report thoroughly before applying for a loan. When talking to your lender, confidently state that you’ve carefully examined your credit and highlight any positive aspects, such as a history of timely payments.

2. “I don’t have any savings for a down payment.”

While it’s true that not all mortgage programs require a significant down payment, admitting that you have no savings can send the wrong message to your lender. It may raise concerns about your ability to manage future mortgage payments and other financial obligations.

What to say instead: Focus on highlighting other strong financial factors, such as a stable income or a low debt-to-income ratio. If you’re unable to make a sizable down payment, explore alternative options like down payment assistance programs and government-backed loans.

3. “Can you ignore this other loan I have?”

Full transparency is vital when discussing your financial situation with a lender. Asking them to ignore another loan is a major red flag. It suggests that you’re trying to hide certain financial obligations, which can damage your credibility and jeopardize your chances of getting approved for the mortgage.

What to say instead: Be honest about all your existing debts and financial commitments. Instead of asking the lender to ignore the other loan, focus on explaining how you plan to manage multiple obligations responsibly, demonstrating your ability to handle the new mortgage.

4. “I’m planning to quit my job soon.”

Stability is a key consideration for mortgage lenders. When you mention your intention to quit your job in the near future, it raises concerns about your ability to make consistent mortgage payments. Lenders prefer borrowers with a steady employment history.

What to say instead: Emphasize your employment stability and provide a clear picture of your long-term career plans. Lenders want to see that you have a reliable source of income, so if changing jobs is necessary, it’s best to secure new employment before applying for the loan.

5. “Can we work around the income I get under the table?”

Seeking to work around the income you receive “under the table” or off the record is a risky proposition. It’s important to note that mortgage lenders require documented income for loan approval. Asking them to consider undocumented income raises ethical and legal concerns.

What to say instead: Focus on highlighting your verifiable sources of income. While it may not include the “under the table” earnings, stressing your overall financial stability can strengthen your loan application.

6. “I have a great investment opportunity I can’t pass up.”

When you mention a “can’t pass up” investment opportunity to your lender, it can make them question your financial priorities. They want to ensure that you have sufficient funds to cover the mortgage and any related costs. Expressing a strong desire to divert funds to other ventures may raise doubts about your ability to meet your financial obligations.

What to say instead: Emphasize your commitment to the mortgage and your understanding of the financial responsibilities it entails. If the investment opportunity is time-sensitive, consider discussing a plan for taking advantage of it after securing the loan.

7. “I’m not interested in shopping around for rates.”

Securing the best mortgage deal is often a result of diligent rate shopping. When you express disinterest in exploring other options and accepting the first offer, it can signal to the lender that you may not be fully informed about the mortgage process or are willing to accept higher rates.

What to say instead: While expressing a desire for a convenient and efficient loan process, convey your intention to explore competitive rates from other lenders. This shows that you are a proactive borrower, committed to finding the best mortgage terms.

8. “Sorry, I exaggerated a bit on my application.”

Integrity and honesty are non-negotiables in the mortgage application process. Admitting to exaggerating or providing false information on your application can have severe consequences. It can lead to immediate rejection or, if discovered later, result in the cancellation of the loan.

What to say instead: Take the time to carefully review all the information in your application. If you find any errors, address them proactively with your lender, ensuring that you provide accurate and updated details.

9. “I’m not a fan of paperwork. Can we skip some of it?”

Mortgage applications require a significant amount of paperwork for a reason. It helps lenders assess your financial capacity and evaluate the risk associated with the loan. Asking to skip certain documents can be interpreted as a lack of seriousness about the process.

What to say instead: Express your willingness to provide all the necessary documents promptly. If you’re facing challenges in gathering specific paperwork, discuss alternatives with your lender to demonstrate your commitment to meeting their requirements.

10. “My current lender said I should have no problem getting approved.”

While a positive pre-approval or feedback from another lender can boost your confidence, mentioning it to your current lender is not advisable. Each lender has different criteria and evaluates applications independently.

What to say instead: Engage in a discussion focused on the lender’s expertise and their evaluation of your application. This demonstrates your seriousness in considering their services while avoiding any direct comparison or pressure.

Effective Communication With Your Mortgage Lender Is Key

Knowing what not to say to a mortgage lender is just as important as what you say. Remember these tips:

- Be confident in discussing your credit report.

- Highlight other financial strengths if you have no savings for a down payment.

- Be honest about all existing debts; don’t ask the lender to ignore them.

- Emphasize employment stability and long-term career plans.

- Focus on verifiable income; avoid mentioning income received “under the table.”

- Show commitment to the mortgage, even if you have other investment opportunities.

- Express a desire to explore competitive rates.

- Never admit to exaggerating on your application.

- Be willing to provide all necessary paperwork.

- Avoid mentioning positive feedback from another lender.

Remember, your mortgage lender is your partner in the home loan process. Open and honest communication will pave the way for a successful and smooth journey towards your dream home.

Key Takeaway

Applying for a mortgage is a significant financial step, and the words you use when talking to a lender can either help or hinder your progress. Knowing what not to say to a mortgage lender is essential for avoiding potential pitfalls.

Remember, confidence and clarity are crucial when discussing your financial situation. Focus on your strengths and what you can bring to the table, and always be honest and transparent.

Secure your dream home with the right mortgage lender!

When applying for a mortgage, it’s essential to have a skilled Dillon mortgage broker by your side. Contact Cedar Home Loans today and let them help you find the perfect mortgage for your dream home!