Buying a home is an exciting milestone, but it also means taking on a significant financial responsibility. Unless you’re in the fortunate position to purchase a home outright, you’ll likely need to secure a mortgage.

A mortgage is a loan provided by a lender to help you finance your home purchase. Like other loans, mortgages have a specified term within which you need to repay the borrowed amount plus interest. But have you ever wondered how long does a mortgage last? Let’s dive into the details of mortgage length and its various aspects.

What is Mortgage Length?

Mortgage length, as the term suggests, refers to the duration or term of your mortgage loan. It represents the agreed-upon timeline for repaying the borrowed amount in full. Mortgages can have different lengths, ranging from a few years to several decades, depending on the borrower’s financial situation and preferences.

When you secure a mortgage, you and the lender enter into a contract that outlines the terms and conditions of the loan, including the mortgage timeline. This agreement specifies the number of years you have to repay the loan, the interest rate, and other relevant details.

It’s essential to understand that mortgage duration and mortgage length are interchangeable terms and refer to the same concept—the time you’ll spend repaying your mortgage.

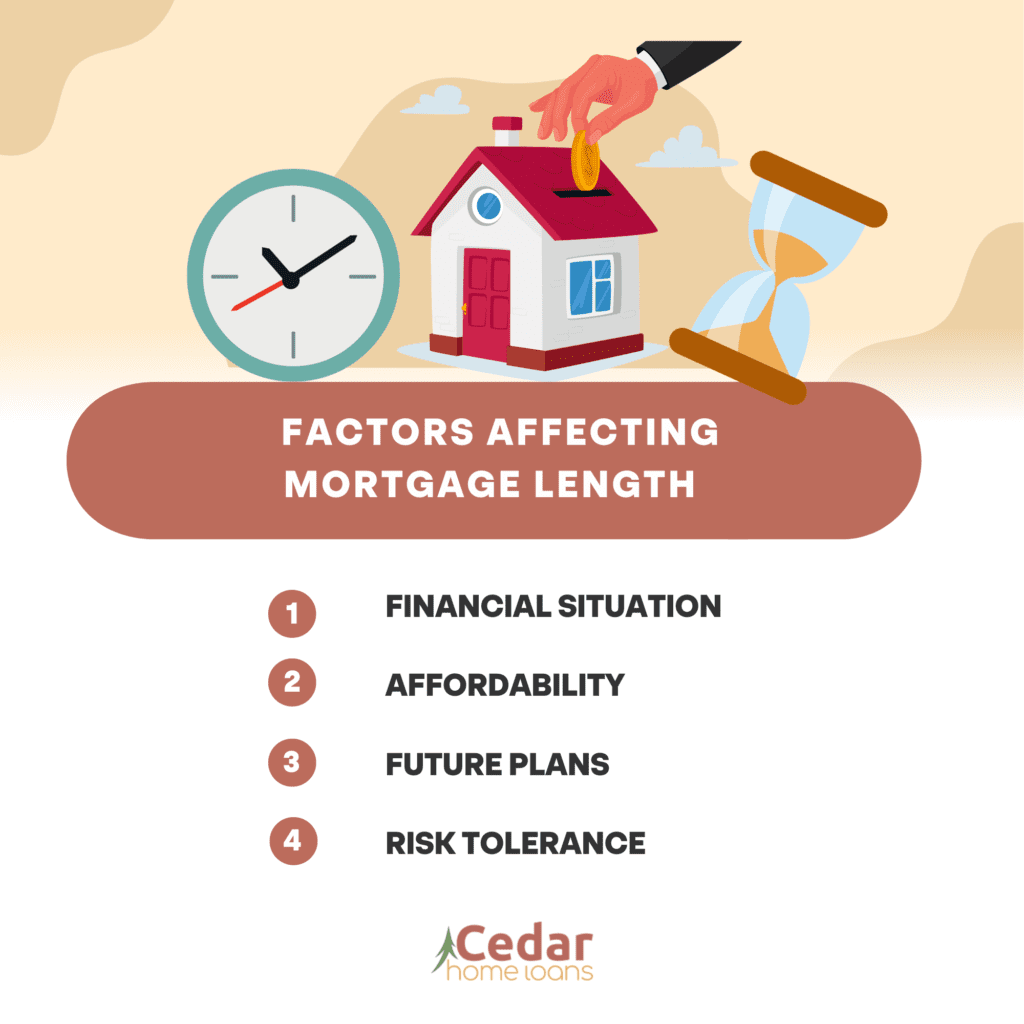

Factors Affecting Mortgage Length

Choosing the right mortgage duration is a significant financial decision since it affects your monthly payments and the overall cost of the loan. Several factors can influence the mortgage timeline you opt for, including the following:

1. Financial Situation

Your financial situation plays a crucial role in determining the duration of your mortgage. It includes factors such as your income, debt-to-income ratio, and credit score. These elements help the lender assess your ability to make timely mortgage payments.

If you have a stable income and a good credit score, you may qualify for shorter-term mortgages, such as 15-year or 20-year options. On the other hand, if you have a lower credit score or higher debt-to-income ratio, you may be more suited for longer-term mortgages, like 30-year ones.

2. Affordability

Another crucial consideration when deciding on a mortgage duration is your affordability. This is determined by the amount of down payment you can make and the monthly payment you can comfortably handle.

Typically, shorter-term mortgages have higher monthly payments but lower interest rates. In contrast, longer-term mortgages often have lower monthly payments but higher interest rates. If you can afford higher monthly payments, a shorter-term mortgage may be a good choice as it can help you save on interest in the long run.

3. Future Plans

Your future plans can also impact the mortgage timeline you select. Consider how long you intend to stay in the home you’re purchasing. If you plan to move in the near future, a shorter-term mortgage might be more suitable, as it can help you build equity faster.

On the other hand, if you plan to stay in the home for an extended period, a longer-term mortgage can provide stability, as you won’t have to worry about refinancing or securing a new loan in the short term.

4. Risk Tolerance

Decisions about mortgage duration also involve risk assessment. Shorter-term mortgages, while potentially saving on interest, can be riskier because of the higher monthly payments. You’ll need to ensure that you can comfortably meet these payments over the short term.

Longer-term mortgages, on the other hand, offer more financial flexibility as the monthly payments are lower. However, they come with the risk of paying more interest over time. Your risk tolerance, therefore, becomes a crucial factor in determining the most appropriate mortgage timeline for you.

Types of Mortgages and Their Duration

The duration of your mortgage can also be influenced by the type of mortgage you choose. Different loan programs have their own set of terms and conditions, which can affect the available mortgage timeline options. Here are some common types of mortgages and their typical duration:

1. Conventional Mortgages

Conventional mortgages are home loans that aren’t insured or guaranteed by the government. They often offer a wide range of mortgage duration options, including 10-year, 15-year, 20-year, 30-year, and even 40-year terms. The most common mortgage length chosen by borrowers, however, is the 30-year option.

2. FHA Loans

The Federal Housing Administration (FHA) insures FHA loans, which are designed to make homeownership more accessible, particularly for first-time buyers. These mortgages typically have more flexible credit requirements and offer mortgage timeline options of 15 years and 30 years.

3. VA Loans

VA loans are mortgages backed by the U.S. Department of Veterans Affairs and are available to eligible veterans, active-duty service members, and surviving spouses. These loans often come with competitive interest rates and can provide mortgage duration options of 15 years and 30 years.

4. USDA Loans

The U.S. Department of Agriculture guarantees USDA loans, which are primarily offered to encourage rural and suburban homeownership. These mortgages typically have a single mortgage timeline option of 30 years.

5. Adjustable-Rate Mortgages (ARMs)

Adjustable-rate mortgages (ARMs) are loans with interest rates that can change over time. They usually have an initial fixed-rate period, typically lasting 5, 7, or 10 years, after which the rate adjusts annually based on market conditions.

6. Jumbo Loans

Jumbo loans are mortgages that exceed the loan limits set by government-sponsored enterprises (GSEs). The duration of your mortgage for jumbo loans can vary, depending on the lender and your financial profile. They often offer mortgage timeline options similar to conventional mortgages, ranging from 15 to 30 years.

Pros and Cons of Different Mortgage Timeline Options

Understanding the pros and cons of different mortgage timeline options can help you make an informed decision when choosing the duration of your mortgage. Let’s explore the benefits and considerations for both short-term and long-term mortgages:

Short-Term Mortgages

Mortgage length options of 10 to 15 years fall under short-term mortgages. Here are their advantages and disadvantages:

Advantages:

- Build equity quickly: Short-term mortgages typically have higher monthly payments, allowing you to build equity at a faster rate.

- Pay less interest: With shorter-term mortgages, you’ll pay less interest over the life of the loan, resulting in significant savings.

- Be debt-free sooner: Paying off your mortgage in a shorter time frame can free up your finances and give you the opportunity to allocate funds to other financial goals.

Considerations:

- Higher monthly payments: The shorter the mortgage timeline, the higher the monthly payments. Ensure that you can comfortably afford these increased payments.

- Stricter qualification: Short-term mortgages often require higher credit scores and lower

The Bottom Line

Deciding on the mortgage length is an important aspect of home financing. It’s a commitment that will significantly affect your financial journey in the coming years. Although there is no one definitive answer to the question of how long does a mortgage last, understanding the various factors of a mortgage timeline can help you make a well-considered decision.

Secure Your Dream Home with CHL!

Are you looking for a reputable Eagle mortgage company to help you get your dream home? At Cedar Home Loans, we offer a wide range of mortgage options tailored to your needs. Get in touch with us today!