Excited about purchasing your first home? Another equally important question, is your wallet getting as excited as you are about this purchase? As a prospective house purchaser, financial readiness is a vital first step to becoming a responsible homeowner. Following this first time home buyer guide, you can take proactive steps to prepare for this lifetime investment!

Know Your Budget

Knowing your budget when buying a house may not be the most exciting part of buying your first home, but it’s the only way to get an idea of your available home-buying options. With a deeper understanding of your budget, you’ll be able to avoid overspending, narrow down your choices, and keep your finances in check. So, before you start dreaming of that walk-in closet or outdoor spa, make sure to become more familiar with your available finances.

Once you know your budget, the harder part may be to adhere to that budget strictly. With all of the available options out there, sticking to your budget may sound as easy as resisting the urge to eat the last spoonful of ice cream. We all know that it’s not that simple; it requires discipline, creativity, and attention to detail when calculating your expenses.

You are effectively tasking yourself to deplete your budget in a way that doesn’t sacrifice your happiness or sanity. Resourcefulness is a must for budgeting, and that may mean finding ways to cut corners and embracing the joy of simple pleasures. This may seem like basic information for first time home buyers, but it is nonetheless critical to have a clear understanding of your financial limits, and to follow those limits accordingly!

Evaluate Your Credit Score

Now it’s time to become the inner detective you are and uncover the secrets hidden in your credit history! Your credit history is your badge of financial honor; it portrays to others your financial trustworthiness and, naturally, the higher your credit score, the more likely you’d be able to secure the help of a lender.

Nine times out of ten, your eligibility for loans, credit cards, and mortgages to finance your home will require a decent level of credit. Investigate your credit history, and if it needs work, try to improve it before deciding to buy a home.

This can be done by having on-time payments on your borrowed credit and limiting your number of new credit accounts. Raising your credit score can open doors to better loan terms, lower interest rates, and higher chances of getting approved for mortgages. Your credit might just be the key to buying your first home, so you want to make sure that you can boast about your credit score loudly and proudly to lenders!

Assess Your Savings

Your savings are your safety net, ready to catch you from any financial impact you’ve taken. The more you put into your savings, the larger and more durable your net is. Keeping your savings accounts properly cushioned is your ticket to financial stability.

Buying your first home will present a plethora of expenses that will readily deplete your savings. Purchasing the home is one thing, but is your savings account going to save you when ongoing expenses rear their head? Things like home repairs or unexpected emergencies should be expected when buying your home, among many other miscellaneous expenses.

Even if the entire process goes smoothly, it still never hurts to keep your savings account properly padded. A sufficiently populated savings account is one of the many resources for first time home buyers that should not be overlooked.

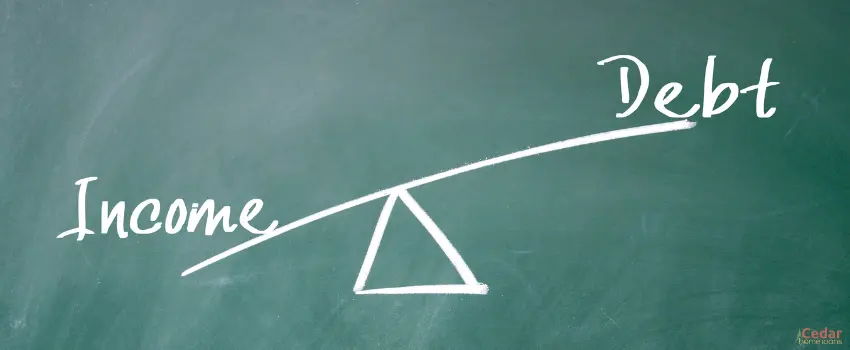

DTI Ratio

Your DTI, or debt-to-income, ratio is exactly what it sounds like – it is a balancing act between the income you make and the debt you’re responsible for. Lenders may analyze this when determining your eligibility for a loan.

To impress lenders better and convince them to provide you with financial assistance, it may be necessary to find ways to increase your income while, at the same time, paying off your debts. This can become a lengthy process, especially if you own many accounts that are in debt, but it is worth improving as it will open the door for more opportunities for buying your first home!

Understand All Costs of Buying a Home

There are numerous costs associated with buying a home that go beyond the price of the home itself. It’s important to remember that you’ll likely incur additional expenses during the entire home-buying process. So, even if you have a budget in mind for the home’s purchase price, expect to be shelling out more to cover extraneous costs.

One such cost would be closing costs. These costs cover the fees for aspects such as a house appraisal, legal paperwork, and title searches, and these costs can easily lead to thousands of dollars.

Other such costs include down payments and monthly mortgages. If you provide a significant down payment on your house, your monthly mortgage may be lessened, and these payments typically include things like property taxes and homeowners insurance fees.

It’s important to have a clear understanding of all the costs associated with buying a home, including both the upfront expenses such as closing costs and down payments, as well as ongoing expenses such as monthly mortgage payments and maintenance costs. It’s always better to be financially prepared and have enough capital to cover these costs, rather than finding yourself in a difficult situation with unexpected expenses down the line.

Key Takeaway

This first time home buyer guide should provide you with an idea of what you can do to prepare for your future home. There are many components to mull over, and you want to make sure that you financially prepare yourself so that you won’t be surprised by the final price tag and other ongoing costs associated with buying a home.

With this information for first-time home buyers, you can approach the house-buying process with a renewed sense of confidence and a clearer understanding of how to finance your new dream home!

Looking for an affordable home loan? Reach out to Cedar Home Loans today!

Whether you’re a first-time home buyer or looking to finance another home, our Vail home loans can help make your dream home a reality!