Investing in your home is a smart decision, as it can increase its value and enhance your living experience. However, not everyone has the financial means to fund their desired home improvements. This is where home improvement loans come into play. They provide the necessary funds for you to upgrade your home, but the question remains: are home improvement loans hard to get?

If you want to upgrade or renovate your home, a home improvement loan is the appropriate loan product for you. They can be obtained through various lenders, including banks, credit unions, and online lenders. Different lenders have varying requirements and some requirements depend on the type of loan you choose.

Home loans are either secured or unsecured. Secured loans require collateral. Often, these come in the form of your home or other valuable assets. Since they have a collateral, the interest rate is usually lower and higher borrowing limits. On the other hand, while unsecured loans do not require a collateral, they may have higher interest rates and stricter eligibility criteria.

Let’s explore how home improvement loans work and the different types available to homeowners.

How Do Home Improvement Loans Work?

Home improvement loans work similarly to other types of loans. Once you qualify for a loan and receive the funds, you can use them to finance your home improvement project. Watch out for different interest rates, repayment terms and other items that are affected by the type of loan you choose and the lender’s requirements.

Some lenders may disburse the loan amount in a lump sum, while others may offer a line of credit or allow for staged payments as the project progresses. It’s essential to choose a loan structure that aligns with your specific renovation plans and financial needs.

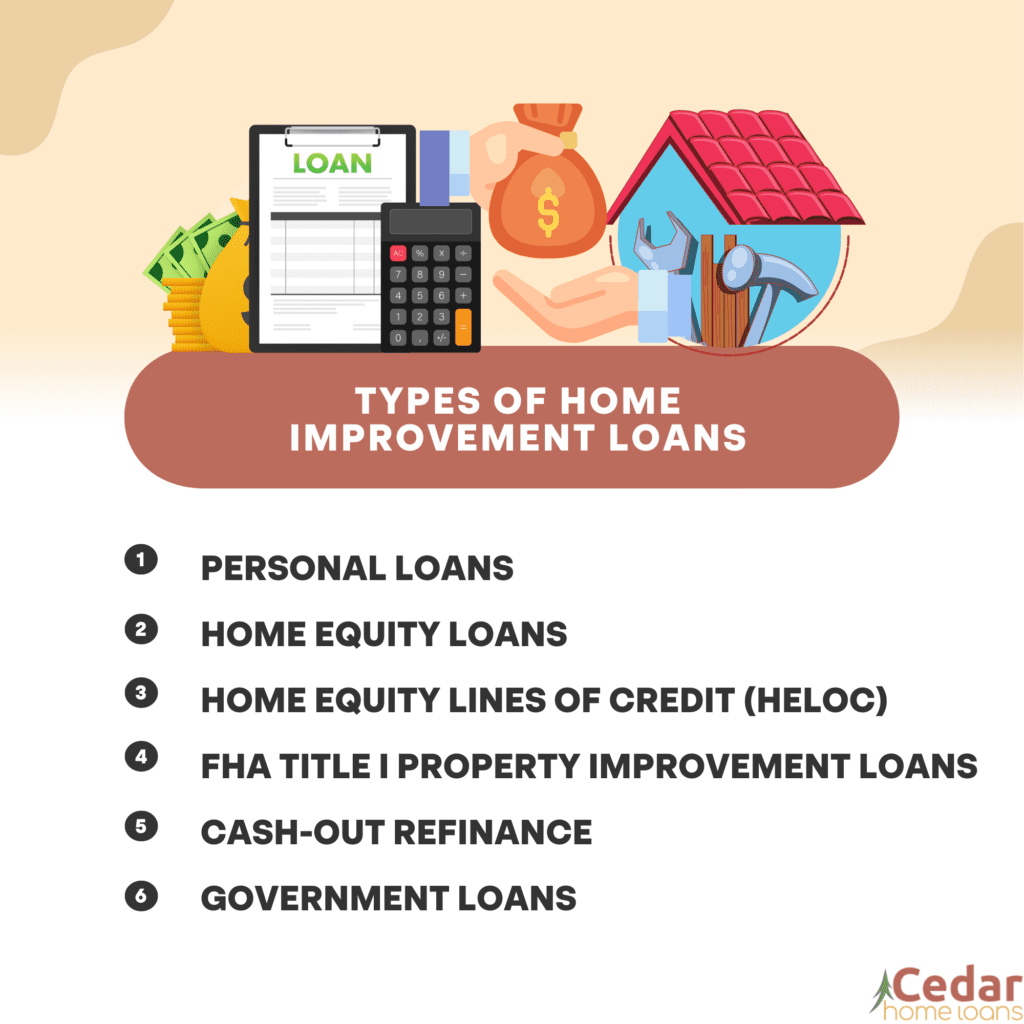

Types of Home Improvement Loans

There are several types of home improvement mortgage loans to consider:

1. Personal Loans

Personal loans are a type of unsecured loan that can be used for various purposes, including home improvements. Creditworthiness, income, and debt-to-income ratio are important aspects in a loan application. The interest rates and loan terms will depend on your credit profile and the lender’s terms.

2. Home Equity Loans

This is also known as a second mortgage which allows you to borrow against the equity you have in your home. It’s a lump-sum loan with a fixed interest rate, repayment term, and monthly payment. To qualify for a home equity loan, you’ll need a significant amount of equity and a good credit score.

3. Home Equity Lines of Credit (HELOC)

This is a revolving line of credit that works similarly to a credit card. You can borrow up to a certain limit, known as your credit limit, and make withdrawals as needed during the draw period. The draw term is usually up to 10 years , during which you only pay interest on the amount withdrawn. To qualify for a HELOC, you’ll need to have equity in your home and a good credit score.

4. FHA Title / Property Improvement Loans

The Federal Housing Administration (FHA) offers these loans to homeowners who need to make repairs or renovations but have little or no home equity. These are insured by FHA. As a result, you can expect better terms such as lower down payments and flexible requirements.

5. Cash-Out Refinance

This arrangement replaces your existing mortgage with a new one. This is usually done when you apply for a loan with an amount higher than your existing loan obligation. The lender will give you the difference between your old loan and new loan in cash. You can use this amount for your home improvement project. Cash-out refinances are best suited for homeowners with substantial equity and good credit.

6. Government Loans

Government loans, such as VA loans and USDA loans, offer eligible homeowners the opportunity to finance home improvements as part of their mortgage. These loans have specific requirements and are tailored to certain individuals, such as veterans or those in rural areas.

Are Home Improvement Loans Hard to Get with Bad Credit?

When you have bad credit, it’s hard to secure a loan but it is not impossible. Many lenders offer options specifically for borrowers with less-than-perfect credit. Expect home improvement loans for bad credit to have a higher down payment requirement and less favorable terms, such as a lower loan amount or a co-signer.

Additionally, some government programs and non-profit organizations provide assistance for home improvements to individuals with bad credit. These programs focus on factors other than credit history, such as income and the ability to repay the loan.

The Bottom Line

If you’re considering a home improvement project but don’t have the funds, there are various loan options available to you. The difficulty of obtaining a loan is influenced by your credit score, the amount of equity you have in your home, and the specific requirements of the lender.

It’s important to shop around and compare loan terms. Gather all the necessary information from different lenders and see what will work best for you. While some loans may be more challenging to qualify for, there are options for every homeowner, including those with bad credit.

Remember, securing a home improvement loan is just the first step. The ultimate goal is to use the funds wisely and create a home that will make you happy.

Get the Home of Your Dreams With Cedar Home Loans

At Cedar Home Loans, we understand that finding the right loan for your dream home can be a daunting task. That’s why our team of experienced and dedicated Frisco mortgage lenders is here to guide you every step of the way. We can help you make the best financial decisions even if this is your first time purchasing a home. Contact us today!