Buying a house is a primary life goal for many people, but it can also be expensive, and most people need more cash to purchase a home with one payment. Consequently, most home buyers will take out a mortgage to help fund their home purchase.

Mortgages can offer many advantages, including:

- Build Equity Over Time – Making monthly mortgage payments is equivalent to building equity in your home. This means that you own a larger share of the property, and your loan balance decreases.

- Tax Benefits – In some cases, you may be able to deduct mortgage interest and property taxes from your income taxes. This can save you money on your taxes each year.

- Stability – Homeownership can provide a sense of stability and security. You have a place to call your own, and you are not subject to the whims of a landlord.

- Appreciation – Over time, the value of your home may appreciate. This means that you could potentially sell your home for a profit.

You will undergo several steps before approval when applying for a mortgage loan. One of the most vital steps is the mortgage underwriting process, which affects your approval status. If you’re wondering what is mortgage underwriting and how the underwriting process for home loans works, let this blog be your guide.

What is mortgage underwriting?

Mortgage underwriting involves lenders viewing your home loan application to assess if it would be safe to lend you money. During this process, the lender will review your application and check your credit-worthiness to guarantee that you’ll be able to repay your loan.

Lenders may have varying loan application forms and document requirements. However, as a general rule you will be asked to provide the following:

- Federal tax returns

- Recent bank statements and proof of other assets

- Proof of other sources of income

- ID and social security number

- Real estate property information

- Details on long-term debts like student loans or car loans

- Employment history

- Assets

- Credit history

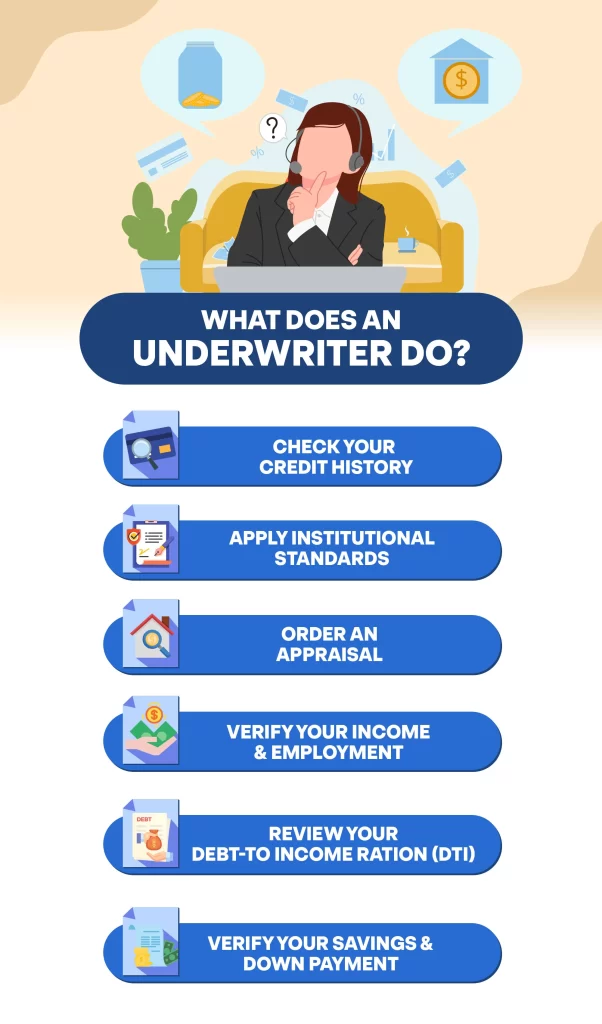

What does an underwriter do?

The mortgage underwriter will go through several steps to evaluate your application before approving or rejecting your loan. The duties of a mortgage underwriter include:

- Check your credit history. They will investigate your payment history and credit score. Things that could affect your credit scores include bankruptcies, late payments, and overuse of credit mechanisms.

- Apply institutional standards. Different lender companies follow specific federation guidelines when reviewing loan applications.

- Order an appraisal. The mortgage underwriter will send an appraiser to the property you’re buying to ensure its value matches the lender’s offer.

- Verify your income and employment. The underwriter will ask for your proof of income and employment. This could be a certificate of employment or a salary slip.

- Review your debt-to-income ratio (DTI). The DTI ratio indicates your spend-to-income ratio. The mortgage underwriter will examine your incoming and outgoing cash flow and determine if your cash flow is sufficient to cover your mortgage payments, insurance, and taxes.

- Verify your savings and down payment. The mortgage underwriter will check your accounts to ensure you can pay for a down payment or enough savings to supplement your income.

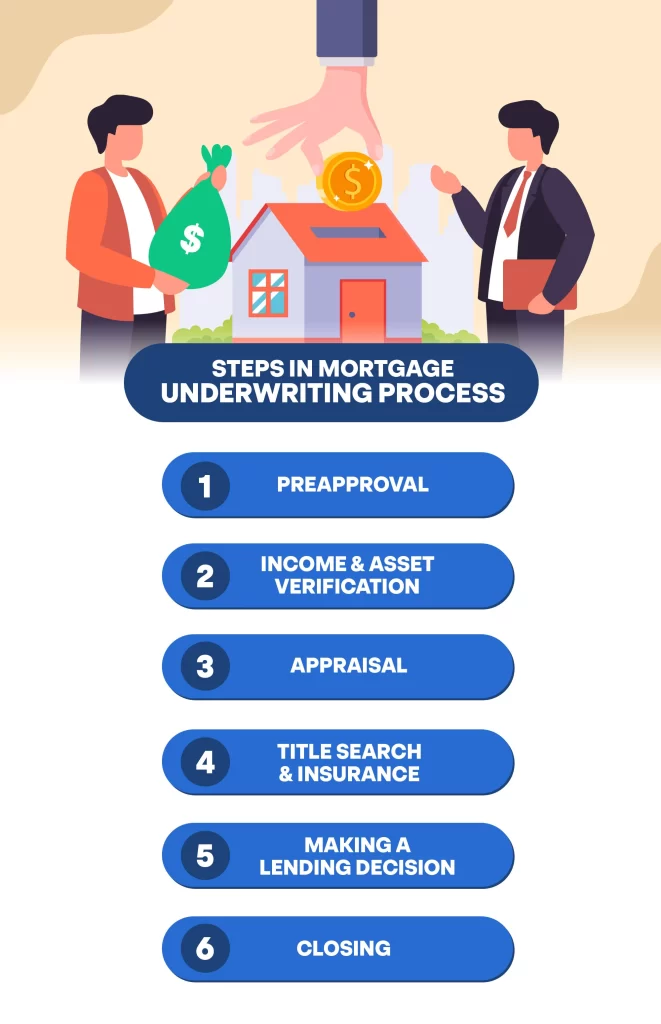

Steps in the Mortgage Underwriting Process

After receiving your requirements, the underwriting process starts. This process could take a long time, and each lending company uses different methods, but here are the five major steps buyers can expect during the underwriting process for home loans.

1. Preapproval

As mentioned, the underwriter will review your financial profile at the start of the mortgage underwriting process. During the pre-approval process, the underwriter will run a credit check to determine if your income matches what you’ve included in the report. They will also check with your employer to verify your employment.

If you are self-employed or own a share in a business, you will need to provide documents like W-2s, profits and loss sheets, K-1s, balance sheets, and tax returns.

In some cases, the mortgage underwriter may use the property as collateral for the loan. Using the property as collateral means that the lender can foreclose on the property if the borrower defaults on the loan. Typically the underwriter will only approve a loan if the amount of the loan does not exceed the value of the property. This ensures that the lender is adequately protected in the event of a default.

2. Income and Asset Verification

The mortgage underwriting process involves verification of financial documentation like bank account statements, investment accounts, retirement savings, and the cash value of your life insurance policies and business ownership assets like stocks and retirement accounts.

Once you are deemed qualified, the underwriter will send you a pre-approval letter that includes the amount you indicated in the application and a statement deeming you fit for a loan.

3. Appraisal

Appraisals are essential to the mortgage underwriting process as they protect all parties concerned. When assessing a home’s value, the appraiser will examine the property to inspect its condition and features. This way, they can determine if the home’s value matches the asking price.

The appraiser will take measurements and pictures to compare them with similar properties in the same location. The underwriter will suspend your application if the property’s appraised value is significantly lower than the mortgage.

4. Title Search and Insurance

Title search and insurance are both part of the mortgage underwriting process steps. Typically they will involve checking if the property’s titles have legal or transferable claims. A title company should research the property’s history and check if it has claims, easement rights, zoning ordinances, mortgages, unpaid taxes, and restrictive covenants. After the research, the title insurer will issue an insurance policy to verify their findings’ accuracy.

5. Making a Lending Decision

The final step in the mortgage underwriting process is waiting for your application’s decision and the outcome. Outcomes could vary in different ways:

- Approved – Your approval could either be “clear to close” or “conditional,” with the latter including certain conditions like providing signatures, tax forms, or prior pay stubs.

- Denied – Denied applications could mean having a low credit score or too much debt. Sometimes, it could also mean you’re not eligible for a particular loan.

- Decision pending – There might be insufficient information for the underwriter to evaluate in pending decisions. It could be they can’t verify your income or employment. This doesn’t mean you are automatically denied; you must provide the missing documents.

6. Closing

You will receive a closing disclosure (CD) from the lender when your application gets approved. The CD will include the terms, your projected monthly payments, and final costs. It’s crucial to examine carefully and review the terms so you can raise questions should any concerns arise.

How long does underwriting take?

The duration of the mortgage underwriting process varies and depends on a case-by-case basis, but the average could take a few days to several weeks. It also depends on how soon all necessary documents are submitted to the underwriter.

Tips for Smooth Mortgage Underwriting Process

To ensure that your experience during the mortgage underwriting goes smoothly, you can follow these simple tips:

1. Organize your documents.

Organizing all your financial documents before applying for a loan is a fast way to improve your mortgage underwriting process. Organizing your documents lets you have the necessary paperwork and documents ready upon the underwriter’s request.

2. Be upfront with your finances.

If you have a low credit score, it can be more difficult for you to get approved for a mortgage—this could also make your loan have a higher interest rate. To increase your credit score and DTI ratio, repay all your debt. Avoid taking on new debt and making other significant financial changes like closing credit cards or other accounts.

3. Stay in touch with your lender.

Throughout the entire underwriting process, the underwriter will consistently ask for paperwork and information. To avoid delays in the mortgage underwriting process, ensure you respond quickly to the underwriter.

Conclusion

The underwriting process is a critical part of the mortgage loan process because it helps the lender determine eligibility, it ensures that the borrower can repay the loan, and it protects the lender from financial losses in the event of a default.

During this process, the underwriter will go through several mortgage underwriting process steps. For example the mortgage underwriter will review your employment history, credit score, DTI, and other financial information to assess your ability to repay the mortgage loan.

After this process, the lender will determine if your application is accepted, denied, or pending. Once approved, you will receive a closing disclosure, including your monthly payment and other terms you can bring up to the lender if you need clarification. It’s crucial to organize your documents, reply consistently to the underwriter, and handle all your finances and debts to ensure your underwriting process goes smoothly.

Buying a new home? Apply for a housing loan from Cedar Home Loans today!

If you’re a first-time home buyer or buying another one, our Colorado mortgage company can help you make that purchase. At Cedar Home Loans, we offer mortgage solutions that can bring you a step closer to buying your dream home. Contact us to learn more about our services so we can help you fund your property purchase!