When it comes to mortgages, there are many terms and concepts to understand. Two of the most important are loan servicers and lenders. While they both play a role in the mortgage process, their responsibilities and functions are quite different.

If you’re planning to take out a mortgage or are already a homeowner, it’s essential to know the difference between these two entities. This knowledge can help you navigate the mortgage landscape more effectively and make informed decisions about your loan.

To shed light on this topic, we’ll discuss the five key differences between a loan servicer and a lender.

What Is a Mortgage Lender?

A mortgage lender is a financial institution or company that provides funds to borrowers to purchase or refinance a home. When you borrow money from a lender, you enter into a legal agreement, often called a mortgage or a home loan.

The lender can be a bank, credit union, or specialized mortgage company. They evaluate your creditworthiness, income, and other financial factors to determine if you qualify for a loan. If approved, the lender sets the terms and conditions of the loan, including the interest rate, repayment schedule, and loan amount.

As the borrower, you have a direct relationship with the lender throughout the mortgage process, from application to closing. Once the loan is funded, you make monthly payments directly to the lender.

What Is a Loan Servicer?

A loan servicer is a company that manages the day-to-day operations of your mortgage after it is originated or funded by the lender. They act as an intermediary between you and the lender, ensuring that all aspects of the loan are properly administered.

Loan servicers have several responsibilities, including:

- Payment Collection: They collect your monthly mortgage payments, send you statements, and keep track of your payment history.

- Customer Service: If you have questions or need assistance with your loan, the servicer is your primary point of contact. They handle inquiries, provide information, and guide you through the mortgage process.

- Escrow Management: In many cases, the servicer also manages your escrow account, which is used to pay your property taxes and insurance premiums.

- Reporting to Lenders: Servicers provide regular reports to the lender, which include information about your payment status and any significant changes to your loan.

- Default Management: If you fall behind on your mortgage payments, the servicer handles the collection efforts and may offer loss mitigation options, such as loan modification or repayment plans.

How Do Lenders and Loan Servicers Work Together?

Once your loan is originated, the lender may choose to keep it in their portfolio or sell it to an investor on the secondary mortgage market. In the latter case, the lender will transfer the legal rights to the loan while retaining the financial interest in its repayment.

When a loan is sold, the borrower is notified of the transfer by both the lender and the new loan owner. The new owner, often a mortgage investor or a government-sponsored enterprise, then designates a loan servicer to handle the ongoing management of the loan.

It’s important to note that as a borrower, you typically do not have control over the selection of your loan servicer, as this decision is made by the loan owner or investor.

What Are the Key Differences Between Loan Servicers and Lenders?

Now that we’ve defined both parties let’s dive into the differences between loan servicers and lenders.

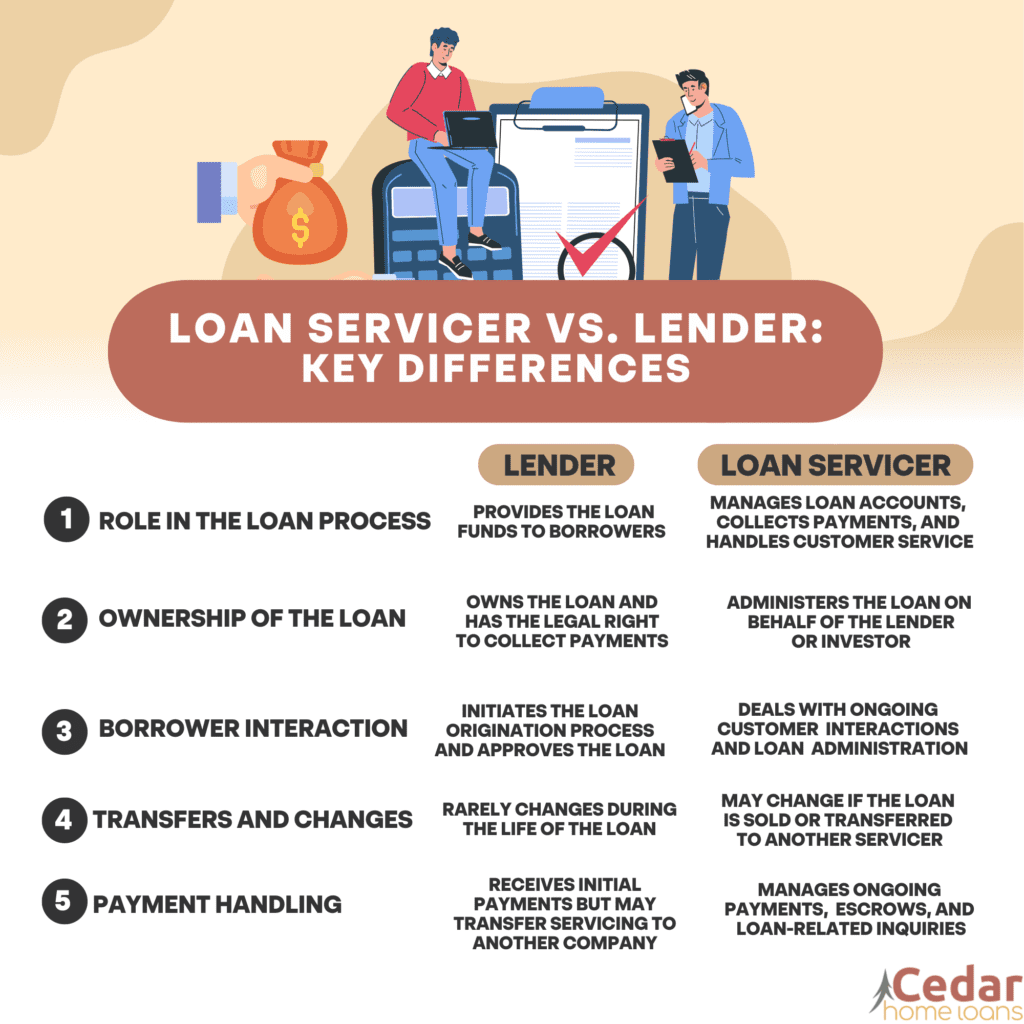

1. Role and Function

The primary role of a lender is to provide the funds for your mortgage. They are the ones taking the financial risk and have a vested interest in the successful repayment of the loan. In contrast, the loan servicer’s role is to manage the administrative tasks associated with the mortgage, acting as a middleman between you and the lender.

2. Customer Relationship

As a borrower, you have a direct relationship with the lender. You communicate with them throughout the mortgage process, and they make the final decisions on your loan, including approval and setting the terms. On the other hand, the loan servicer is your main point of contact for any inquiries or assistance after the loan closes.

3. Ownership of the Loan

The lender owns the loan if they choose to keep it in their portfolio, while the loan servicer takes over the management of the loan on behalf of the new owner if the loan is sold to an investor. In this case, the servicer becomes the face of the loan, handling all interactions and transactions.

4. Decision-making Authority

As the loan owner, the lender has the final say on any significant changes to the loan terms, such as modifications or refinancing. In contrast, the loan servicer may have the authority to make minor administrative changes, but they must obtain approval from the lender for any material amendments.

5. Contractual Obligation

When you borrow money from a lender, you enter into a legally binding agreement, the mortgage contract, which outlines your obligations and rights as a borrower. The loan servicer, as a third-party service provider, is not a party to this contract. Instead, they enter into a separate service agreement with the lender, outlining their responsibilities.

Can a Lender Be a Loan Servicer?

Yes, a lender can also be a loan servicer. In this scenario, the lender chooses to retain the servicing rights, which means they will handle the day-to-day management of the loan. As a borrower, you will continue to make payments directly to the lender-servicer.

Conclusion

Understanding the differences between loan servicers and lenders is essential in navigating the mortgage landscape. While lenders provide the funds and have the ultimate decision-making authority, loan servicers manage the administrative aspects of the mortgage, acting as an intermediary between you and the lender.

Remember that, in most cases, the lender selects the loan servicer, and as a borrower, you have little control over this decision. Therefore, when evaluating mortgage options, it’s crucial to consider the reputation and track record of both the lender and the potential servicer.

Get the Best Mortgage Services!

Looking for a mortgage? Choose the best Boulder mortgage company for your needs! Partner with Cedar Home Loans. We offer a wide range of mortgage solutions. Our team is ready to guide you and answer your questions. Contact us today!